Earnings results often indicate what direction a company will take in the months ahead. With Q4 behind us, let’s have a look at First Solar (NASDAQ:FSLR) and its peers.

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

The 17 renewable energy stocks we track reported a mixed Q4. As a group, revenues missed analysts’ consensus estimates by 4.6% while next quarter’s revenue guidance was 0.6% above.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 8.4% since the latest earnings results.

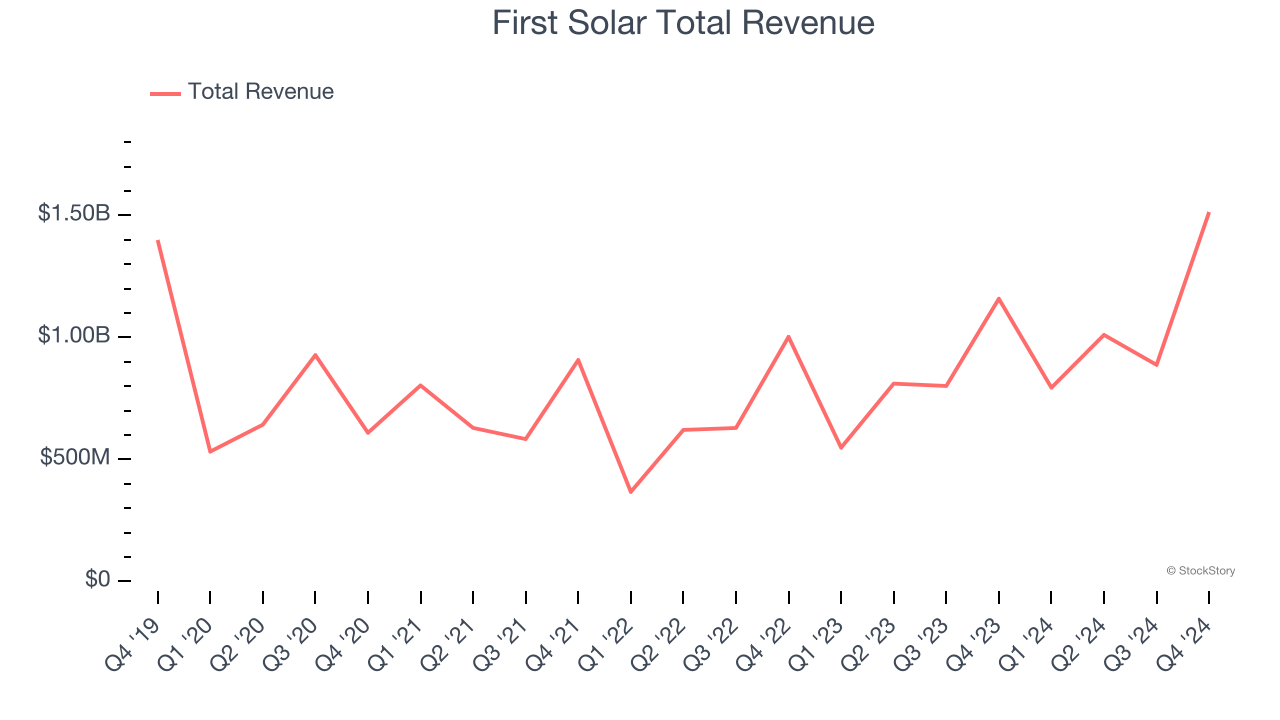

First Solar (NASDAQ:FSLR)

Headquartered in Arizona, First Solar (NASDAQ:FSLR) specializes in manufacturing solar panels and providing photovoltaic solar energy solutions.

First Solar reported revenues of $1.51 billion, up 30.7% year on year. This print exceeded analysts’ expectations by 2%. Despite the top-line beat, it was still a softer quarter for the company with full-year EPS guidance missing analysts’ expectations.

“In 2024, we continued building the foundations required for our long-term growth strategy,” said Mark Widmar, chief executive officer, First Solar.

The stock is down 11.1% since reporting and currently trades at $130.80.

Is now the time to buy First Solar? Access our full analysis of the earnings results here, it’s free.

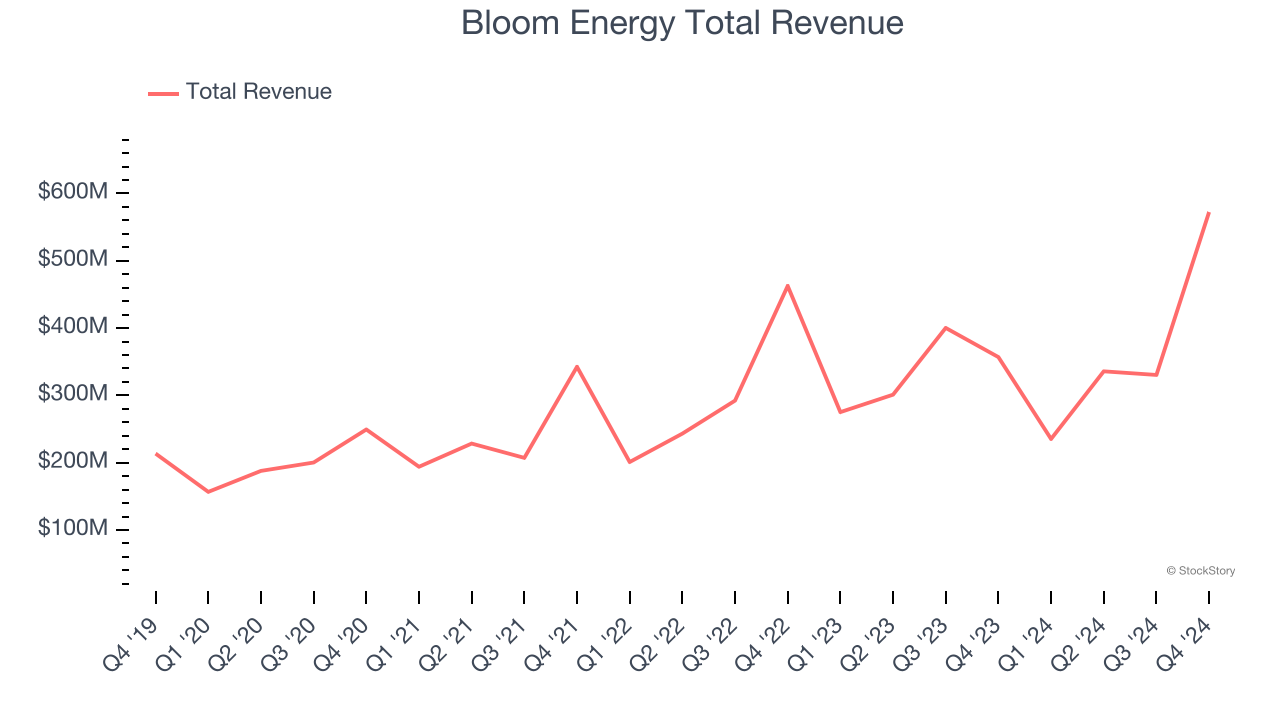

Best Q4: Bloom Energy (NYSE:BE)

Working in stealth mode for eight years, Bloom Energy (NYSE:BE) designs, manufactures, and markets solid oxide fuel cell systems for on-site power generation.

Bloom Energy reported revenues of $572.4 million, up 60.4% year on year, outperforming analysts’ expectations by 12.8%. The business had an incredible quarter with a solid beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

Bloom Energy delivered the biggest analyst estimates beat, fastest revenue growth, and highest full-year guidance raise among its peers. The market seems happy with the results as the stock is up 7.6% since reporting. It currently trades at $24.77.

Is now the time to buy Bloom Energy? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: TPI Composites (NASDAQ:TPIC)

Founded in 1968, TPI Composites (NASDAQ:TPIC) manufactures composite wind turbine blades and provides related precision molding and assembly systems.

TPI Composites reported revenues of $346.5 million, up 16.7% year on year, falling short of analysts’ expectations by 5%. It was a disappointing quarter as it posted full-year revenue guidance missing analysts’ expectations.

As expected, the stock is down 30.1% since the results and currently trades at $1.01.

Read our full analysis of TPI Composites’s results here.

Enphase (NASDAQ:ENPH)

The first company to successfully commercialize the solar micro-inverter, Enphase (NASDAQ:ENPH) manufactures software-driven home energy products.

Enphase reported revenues of $382.7 million, up 26.5% year on year. This number surpassed analysts’ expectations by 1.6%. Aside from that, it was a satisfactory quarter as it also produced an impressive beat of analysts’ adjusted operating income estimates.

The stock is down 6% since reporting and currently trades at $62.29.

Read our full, actionable report on Enphase here, it’s free.

American Superconductor (NASDAQ:AMSC)

Founded in 1987, American Superconductor (NASDAQ:AMSC) has shifted from superconductor research to developing power systems, adapting to changing energy grid needs and naval technology requirements.

American Superconductor reported revenues of $61.4 million, up 56% year on year. This print topped analysts’ expectations by 8.4%. Overall, it was an exceptional quarter as it also put up an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

The stock is down 21.1% since reporting and currently trades at $20.18.

Read our full, actionable report on American Superconductor here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.